The S&P 500 is Due for a Break, the Dollar a Stall to Start 4Q

Talking Points:

- There was little evidence of a speculative rebalance to end the third quarter, but the S&P 500 is due a short-term break

- Following the path of last resistance, the bullish break from the Dollar now requires fundamental reinforcement to continue

- Though trade wars and policy normalization are key systemic themes, monitor targeted volatility for EUR, CAD and CHF

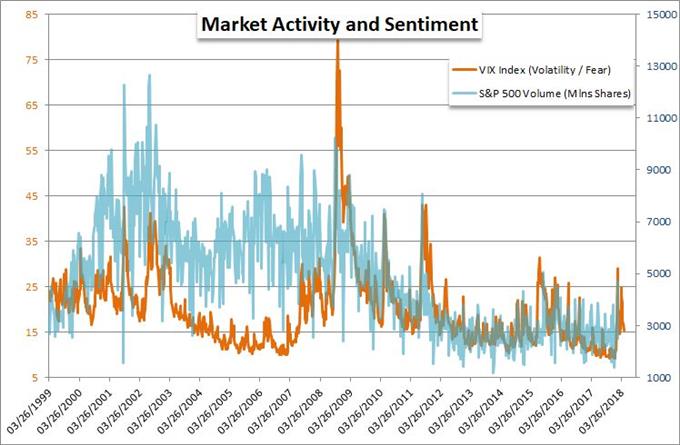

EVALUATING RISK TRENDS AS THE FOURTH QUARTER STARTS

With the close of the past week, we now transition into a new month and quarter. Historically, September represented the worst monthly performance of the calendar year for the S&P 500. That wasn't the case this year - that's why they are called averages. Just as it had in 2017, the top performing risk benchmark charged through another year's statistical trip point unscathed as pushing fresh record highs. Referring to the same norms, October doesn't carry a negative average itself for US equities; but it has far more reliable - and in some ways, systemically more important - norms. From the S&P 500's statistics back to 1980, October registers the heaviest month of volume by far. In other terms, that can be construed as 'participation'. This new month also happens to represent the peak for volatility according to VIX seasonality. Combine volatility and volume and you’re more likely to develop a trend. There is an inherent bias when it comes to volatility's correlation to risk trends, but we don't need to revert to such speculative assumptions. If there is a robust trend to arise, is it going to be a renewed bull trend for US equities already at record highs? Appetite for speculative assets with a discount (like emerging markets) may offer opportunity in a relentless push higher, but the risk-reward balance will always lean against something like the S&P 500. Further, with enormous issues such as trade wars, monetary policy normalizing from extremes and growing political risks; it is clear the potential for sudden momentum.

NOW THAT THE NECESSARY DOLLAR BREAK IS OUT OF THE WAY

This past week, the Dollar made a noteworthy technical break. With the coming week, we will see how potent conviction behind the move is in the market's eyes. On Thursday, the DXY Dollar Index ended a terminal wedge with a break higher that staved off a more ominous break on a medium-term, head-and-shoulders pattern. For EURUSD, that would translate into the failure to launch the 1.1700 breakout to sustainable trend. Yet, when we evaluate the Greenback's performance in a more neutral light - an equally weighted index of the majors - we find that the intraweek charge carried limited speculative intent. It was a move back into range - and ultimately, so too were the jolts from the DXY and EURUSD. This was a break following the 'path of least resistance', simply a means for relieving pressure but not an indication for genuine momentum. Now, the real work starts. If the bulls are taking control of the currency, they will need to muster deeper conviction and rouse more forces. Where would the bulls source their strength moving forward? The monetary policy advantage is one area that serves as a textbook reference, but it has done little to support the currency this past week, the past months and certainly throughout 2017. A systemic risk aversion could leverage the undisputable appeal of the Greenback's liquidity, but that is a development with far more options than just the Dollar. The list of possible risks on the other hand is far longer. Possible flagging of growth and rates is a lingering risk, while trade wars and mid-term election uncertainties are inevitable issues. Beware your expectations for the Dollar; and at the very least, look for significant technical breaks before you support conviction.

THE RETURN OF AN (IGNORED?) EURO CRISIS AND THE SWISS EU HANG UPS

For those that were trading FX or international markets five or more years ago, a familiar fundamental concern is starting to return to the financial headlines: systemic concern over the cohesion of the Euro-area. There has been a tickle of uncertainty the past year through the UK's divorce from the EU, but the threat is starting to circle closer to the Monetary Union that supports the second most liquid currency in the world. Concern over Italy has slowly been building over time, but it hit a different gear this past week after the Populist government pushed ahead with a 2.4 percent deficit-to-GDP ratio for the next three years - a level that has raised a red flag with the European leaders. The Euro dropped on a broad basis for three days through Friday, but this currency and region has a penchant for discounting systemic threats for a complacent slide into a solution. Nevertheless, beware. In the event of a sustained Euro burn, EURUSD is an uneven candidate while EURJPY will add a risk skew to the mix. EURCHF brings its own appeal as a regional risk aversion shift, but the Swiss Franc itself presents a more immediate bearish pressure. An equally weighted CHF index showed a dramatic spill in the second half of this past week in part owing to a standoff on reaching agreement between Switzerland and the European Community.

EASY AND COMPLEX CATALYSTS FOR THE CANADIAN DOLLAR, GOLD FACES STATISTICS EXTREMES

Looking ahead to the coming trading week, there are both themes and targeted event risk for which traders should account. For the Canadian Dollar, it is facing a healthy dose of both. Through the end of the past week, the Loonie posted a broad bullish break on the combination of a monthly GDP beat and reports that the Mexican President-elect wanted a trilateral agreement on the NAFTA replacement before the country participated. With the details of the deal from the US due Sunday and the NAFTA deadline on October 1. For specific data, Friday's combination of monthly Canadian employment and trade figures will leverage a fundamental impact of consequence. Be wary of changing tides given the nature of these catalysts. From fundamentals to statistics, gold is lacking for conviction in further retreat or a systemic recovery. Lasting retreat would likely necessitate a material tightening of global monetary policy as risk trends held firm, but a full bore bull trend likely awaits risk aversion that exposes the dependence on extreme easing by central banks. In the meantime, September closed out a sixth consecutive month decline for the commodity to match the longest tumble since 1997. There are no seven-month retreats on record going back to at least 1970. We discuss some of the key fundamental themes and technical formations for the markets over the coming week, month.

Start Trading with Free $30 : CLAIM NOW $30

VERIFY YOUR ACCOUNT AND GET YOUR $30 INSTANTLY ,MAKE MONEY WITHDRAW !!

IF YOU FACE ANY PROBLEM TO GET THIS OFFER PLEASE CONTACT US FOR

SUPPORT , CLICK SMS BAR ABOVE THEN TALK TO US.

Comments

Post a Comment